The Mid-Market RIA Valuation Gap Is Widening. What Most Owners Don’t See.

In this RIA Perspective for Amplify Platform, Adam Scully-Power, Managing Director of Enterprise Strategy, examines why mid-market RIA firms with comparable AUM and growth profiles are receiving dramatically different acquisition multiples—and why that gap is widening. Drawing on data from DeVoe & Company, Advisor Growth Strategies, ECHELON Partners, and F2 Strategy, Scully-Power argues that PE-backed buyers are now explicitly pricing operational architecture, and that the infrastructure decisions RIA owners make in the next 12 to 24 months will determine their valuation outcome in a sale event that is closer than most assume.

Consider two firms in the same AUM range, call it $3B each, both growing organically, both serving similar client bases, both in good geographic markets. Five years from now, one may sell for 14 times EBITDA. The other may struggle to clear 8 times. The difference between those outcomes is roughly $40 million in enterprise value, and it will not be explained by anything the owners are tracking on their dashboards today.

After thirty years in this industry, I have watched several consolidation cycles play out. The current one is structurally different, and the variable that separates premium outcomes from discount outcomes has shifted in a way most mid-market RIA owners have not internalized yet

The Gap Is Real, and It’s Accelerating

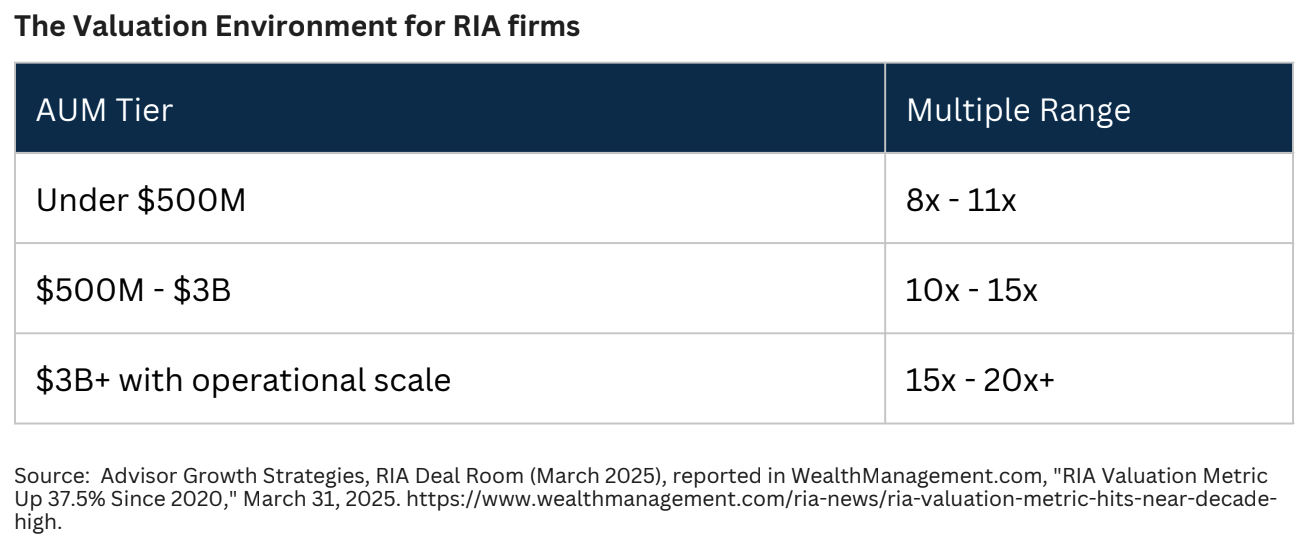

The valuation environment has shifted dramatically. RIAs under $500M in AUM now command multiples ranging from 8x to 11x EBITDA. Firms between $500M and $3B command 10x to 15x. And the most sought-after firms, those with strong organic growth and operational scale, are pulling deals in the 15x to 20x range, with select transactions crossing 20x. That spread, roughly 2x to 3x between premium and discount outcomes for firms of comparable size, is widening, not narrowing.

The dynamic is visible even in headline transactions. When LPL Financial acquired Commonwealth Financial Network in March 2025 for $2.7 billion, the deal was reported at a 22.5x multiple of closing EBITDA. On LPL’s own unaudited adjusted EBITDA basis, the multiple may have been closer to 8.0x. Same transaction, the same target, the same buyer, and a 14 turn gap between the two numbers, depending on what you count as earnings. Headline multiples are not the story. What sits underneath the EBITDA line, the operational profile that determines whether earnings will hold, grow, or compress after integration, is what sophisticated buyers are actually pricing.

Capital is flowing into the sector at a pace that makes these judgments increasingly consequential. The industry recorded 466 announced transactions in 2025, a new all-time high and a 27.3% increase year-over-year, the fastest growth rate in a decade outside the 2021 surge. Every quarter of 2025 exceeded 100 transactions, the first time on record. Financial buyers were involved either directly or as a financial partner to the acquirer in 75.8% of all 2025 transactions, up from 71.0% in 2024 and 62.0% in 2023. Private equity is no longer a meaningful participant in the market. It is the market.

These buyers are not paying uniform multiples. They are paying premium multiples for firms that meet specific operational criteria. They are paying discounted multiples for firms that do not, regardless of AUM size or growth rate. This is the gap. And it is widening because the criteria PE-backed buyers use to determine premium pricing are becoming more sophisticated, not less.

What Most Owners Think Explains It

Ask a mid-market RIA owner what determines their firm’s valuation, and the answers cluster around a familiar set. AUM growth rate. Advisor team quality. Client retention. Geographic market. Fee structure. Brand recognition. These factors matter. They are not wrong. But they are table stakes. Every serious acquirer assumes you have most of them. They drive whether your firm gets a meeting with a buyer at all. They do not drive whether you end up on the premium side or the discount side of the multiple spread.

Mature operating infrastructure is the foundation that lets firms grow revenue, expand EBITDA, and improve margins. The firm becomes structurally more profitable as it grows.

The conventional explanations are themselves caught in the same dynamic. DeVoe & Company reports that only 22% of RIA leaders now say the next generation could afford to buy out founders, down from 38% just four years earlier. Internal succession, once the default exit path, is now financially out of reach for most firms. The valuation premium that should make founders wealthy is the same premium that forces them to sell externally rather than transition internally. The architecture of the firm is what determines whether that external sale produces a premium outcome or a discounted one.

The factor that drives that distinction is one most owners are not measuring and not optimizing for, because it does not show up on standard dashboards. It is not in their financial reporting. It is not in their growth metrics. It is, however, the first thing a sophisticated PE diligence team evaluates when assessing a target.

The Real Variable: Operational Architecture

The variable is operating infrastructure. Specifically, whether the firm can scale revenue faster than it scales headcount.

This sounds abstract until you translate it into the operational reality of running an RIA. A firm with mature operating infrastructure can absorb new advisors, new clients, new custodians, and new product capabilities without proportionally increasing operations headcount, compliance staff, or technology overhead. Revenue grows. EBITDA expands. Margins improve.

The firm becomes structurally more profitable as it grows. A firm with fragmented operating infrastructure cannot. Every new advisor adds operational complexity. Every new custodian creates new reconciliation work. Every new client expansion requires manual data movement between disconnected systems. The firm hires to compensate. Revenue grows, but EBITDA stays flat or compresses. Margins erode. The firm becomes structurally less profitable as it grows.

A firm with mature operating infrastructure can absorb new advisors, new clients, new custodians, and new product capabilities without proportionally increasing operations headcount, compliance staff, or technology overhead … A firm with fragmented operating infrastructure cannot.

This dynamic is now widely recognized within the industry. In a Q1 2026 survey of 36 leading wealth management firms conducted by F2 Strategy, 79% reported they plan to change their operating model within the next 12-24 months. The most cited unmet capabilities were not advisor-facing features but foundational infrastructure: systems integration, data and analytics, product management, change management, and operations process design. The industry knows where the gap is. The question is which firms will close it before the valuation cycle closes the window for repositioning.

In the consolidation cycle of 2010 to 2015, this distinction did not matter much. Buyers paid multiples on revenue and AUM. In the cycle of 2015 to 2020, it started to matter. EBITDA quality entered the conversation. In the cycle we are in now, it is the central variable. PE-backed consolidators are explicitly pricing operational maturity, because the firms they are acquiring are being rolled up into platforms where operational scalability determines the entire investment thesis.

When a PE-backed consolidator pays 15x EBITDA for one $3B firm and 8x EBITDA for another, the difference is rarely about the underlying business quality. It is about whether the operational architecture of the acquired firm can be integrated into the platform without absorbing significant headcount or creating ongoing operational drag.

Why It’s Widening Now

Three things are happening simultaneously that make this gap accelerate. First, PE-backed consolidators are increasingly sophisticated about diligence. Growth has moved to the center of every conversation. In DeVoe & Company’s 2025 M&A Outlook Report, 79% of buyers and 49% of sellers identified growth as their top strategic objective. Buyers are no longer paying for AUM. They are paying for AUM that can grow, scale, and integrate into a larger platform.

ECHELON’s 2025 deal report frames it directly: successful acquirers will increasingly distinguish themselves through “their ability to articulate a compelling value proposition to sellers, supported by succession solutions, employee development pathways, expanded resources, and a clear plan for preserving client service continuity post transaction.” Read that list carefully. Every item on it is an operational capability, not a financial one. The firms that command premium multiples are the firms that have built the operational profile to deliver on all of them.

Second, the cost of building operating infrastructure compounds over time. Firms that started investing in unified operational architecture five years ago are now meaningfully ahead of firms that started investing this year. Not because the technology is dramatically better, but because the data, the integrations, and the process maturity have had time to compound. The gap between early movers and late movers is widening structurally.

Third, the consolidation window is finite, and the clock is more specific than most owners realize. The average holding period for a private equity investor in the finance and insurance services industry is 5.75 years. Carson Group, Edelman Financial Services, and Wealth Enhancement all received investment from at least one of their financial sponsors in 2021 or earlier.

ECHELON’s 2026 outlook explicitly anticipates a wave of mega-recapitalizations as these sponsors approach their target holding periods. The buyers driving today’s market are themselves preparing for their own exits, which means the operational criteria they apply to acquisitions are increasingly shaped by what the next buyer will pay. Firms that have not built the operational profile to command premium multiples by the time they enter the sale process will sell at discount multiples. That outcome is not reversible.

The Mid-Market Inflection Point Is Already Visible

The data on mid-market RIA transactions makes the timing question concrete. Transactions involving firms with at least $1 billion in AUM hit a record 185 in 2025, up 32.1% from 140 in 2024, the third consecutive year of acceleration in this segment. Within the $1B-$10B cohort specifically, 147 firms transacted in 2025, up from 113 in 2024.

The more telling number is the shift in deal structure. Minority transactions, which let owners take partial liquidity while retaining control, dropped from roughly 23% of $1B-$10B transacting firms in 2024 to roughly 13% in 2025. Owners in this cohort are increasingly choosing full or majority sales rather than partial liquidity. They are not testing the water anymore. They are getting out, or they are committing fully to a larger platform.

That shift matters because it changes who the comparable transactions are. Five years ago, a $3B RIA evaluating its valuation could look to a peer group of similar firms doing minority deals, partner buyouts, and internal transitions. Today, that same $3B RIA is being compared to firms that have already chosen to fully integrate into PE-backed platforms, firms whose operational architecture has been explicitly evaluated against what makes integration work. The benchmark has moved. And it has moved toward firms that have already invested in being acquirable on premium terms.

The Strategic Implication

For mid-market RIA owners reading this, the implication is straightforward but uncomfortable. The operational architecture decisions you make in the next twelve to twenty-four months will determine your firm’s valuation outcome in a sale event that, for many firms in this cohort, is closer than commonly assumed.

This is not a technology question. It is a strategic capital allocation question. The owners I am seeing get this right are reframing their thinking. They are no longer evaluating technology purchases as cost decisions, but as enterprise value decisions. They are asking, for every operational investment, does this make our firm more or less attractive to the kind of buyer we want to attract in five years.

The operational architecture decisions you make in the next twelve to twenty-four months will determine your firm’s valuation outcome in a sale event that is closer than you think.

That reframing changes everything. It changes what gets prioritized. It changes how decisions get justified to the board or the partners. It changes which vendors get serious consideration and which get screened out.

The Window

The data from the most recent industry research, from DeVoe, from F2 Strategy, from Advisor Growth Strategies, from ECHELON Partners, all points to the same conclusion that experienced operators have been seeing in their work for some time. The question is no longer whether the operating infrastructure of a firm determines its enterprise value. The question is which firms will reposition before the window closes.

ECHELON projects 2026 deal volume will surpass 2025’s record but stay under 500 transactions, with unique buyers up 17.6% year-over-year. The buyer universe is expanding, the capital is in place, and the largest sponsors are approaching their own liquidity events. Every one of these conditions favors sellers who can present the operational profile a sophisticated buyer wants. None of them favor sellers who cannot.

The mid-market RIA owners who will look back in five years on this period as the moment they built premium enterprise value are the ones making different decisions today than their peers. Not better decisions in the same category. Different decisions in a different category entirely.

The valuation gap is not closing. The owners who can see why are positioning accordingly. The owners who cannot are running out of time to figure it out.

Every operational investment your firm makes in the next 24 months is either building enterprise value or not. The Executive Diagnostic shows you where you stand against the firms commanding premium multiples today. → See where your firm stands

Adam Scully-Power currently serves as Amplify’s Managing Director, Enterprise Strategy

- Notes:

Illustrative example only. Calculation assumes a $3B AUM RIA generating ~$21M in revenue at a 70 bps blended fee rate and operating at an ~32% EBITDA margin, producing ~$6.7M in EBITDA. Applied to a 6x EBITDA multiple spread (14x vs. 8x), the implied enterprise value differential is ~$40M. Actual results vary significantly by firm. Not a projection or prediction of any specific transaction. - Advisor Growth Strategies, RIA Deal Room (March 2025), reported in WealthManagement.com, “RIA Valuation Metric Up 37.5% Since 2020,” March 31, 2025. 1. F2 Strategy, “Q1 2026 Trend Report, Operating Models Require Continuous Evaluation and Improvement”

- ECHELON Partners, 2025 ECHELON RIA M&A Deal Report (published February 2026), Top Deal Timeline & Commentary regarding the March 2025 LPL/Commonwealth Financial Network Transaction.

- DeVoe & Company, 2025 M&A Outlook Report, as cited in Q1 2026 RIA M&A Deal Book.

- F2 Strategy, Q1 2026 Wealth Management Trend Report: Operating Models Require Continuous Evaluation and Improvement.

Contact Us

Have a question?

To learn more about the Amplify Platform and how Amplify can simplify your journey with modern technology that works for you, reach out to connect with our experts today.